CLOB Wars

Can Solana's next move topple Hyperliquid?

Disclaimer: This article is purely for informational purposes, and none of it should be considered as financial or any other advice.

A special thank you to Squid (Drift), Fikunmi (Eclipse), Max Resnick, and Alessandro Decina (Anza) for their help and for reviewing earlier drafts of this article.

Introduction

For years, AMMs like Uniswap and Orca have been the backbone of DeFi, with their algorithmic approach making them easy to design and deploy onchain. But they come with trade-offs like higher fees, poor price discovery, and increased slippage. Now, CLOBs - the gold standard in traditional finance - are gaining traction onchain. Unlike AMMs, CLOBs let traders place custom buy and sell orders at specific prices, enabling more efficient and transparent markets.

In this article, we’ll compare Solana’s evolving CLOB and greater DeFi ecosystem to Hyperliquid’s specialized approach, breaking down technical superiorities, challenges, trade-offs made, and the way forward.

CLOBs, AMMs & more

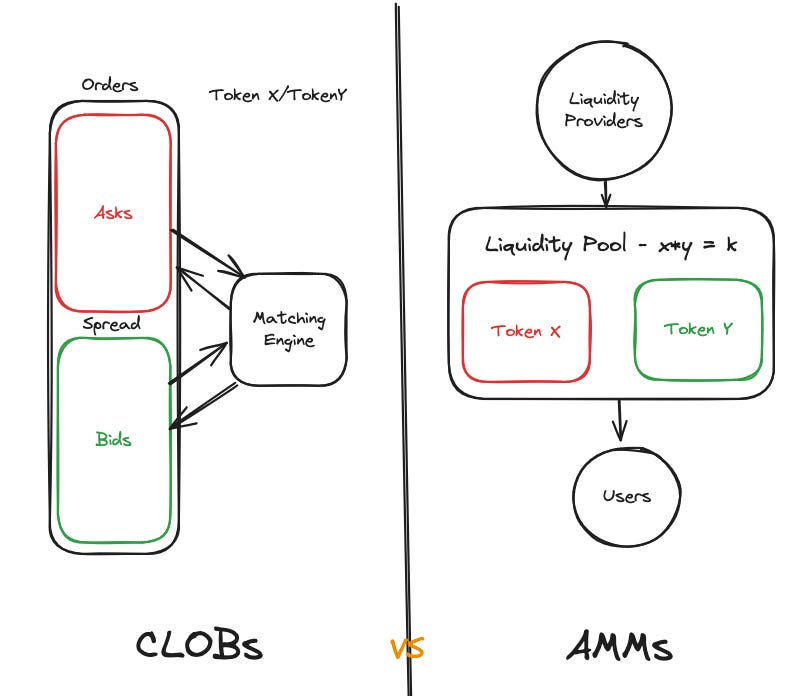

A Central Limit Order Book or CLOB is a traditional exchange mechanism where buyers and sellers post limit orders (with a specified price and quantity), which are queued and matched by price-time priority. The highest bid and lowest ask converge to define the market price, and participants can place orders at any price. This model offers transparent price discovery, allowing users to set custom prices and sizes.

By contrast, Automated Market Makers (AMMs) like Uniswap use liquidity pools and pricing formulas (example: constant-product) instead of order books. AMMs guarantee that any trader can swap against a pool at a price determined by a formula, but at the cost of price impact and less precise control. AMMs are simpler to implement onchain (no orderbook), but they require liquidity providers to deposit tokens and often suffer from slippage on large trades.

Messari Research opines that onchain CLOBs represent the optimal DEX architecture for capital efficiency, price discovery, and scalability, combining the capital efficiency of orderbook matching with transparency. The drawback is they demand low latency and low gas fees to function smoothly onchain - historically a challenge on many blockchains. This means DeFi is relegated to CEX-DEX arbitrage, rather than being the venue for price discovery. CLOBs might not be the endgame for onchain finance, though it will look pretty similar to a CLOB.

Solana getting CLOBbered

Solana’s superiority in throughput and low fees makes it the perfect playground to experiment with different DeFi mechanisms, including CLOBs. Serum DEX was the first iteration launched in 2020 by Alameda Research. It implemented a permissionless onchain CLOB and matching engine. Users placed orders via transactions, and a separate offchain ‘crank’ repeatedly called the matching logic to settle trades. This was a pretty good pilot, but the Solana network was pretty nascent at the time, with suboptimal designs like a FIFO scheduler.

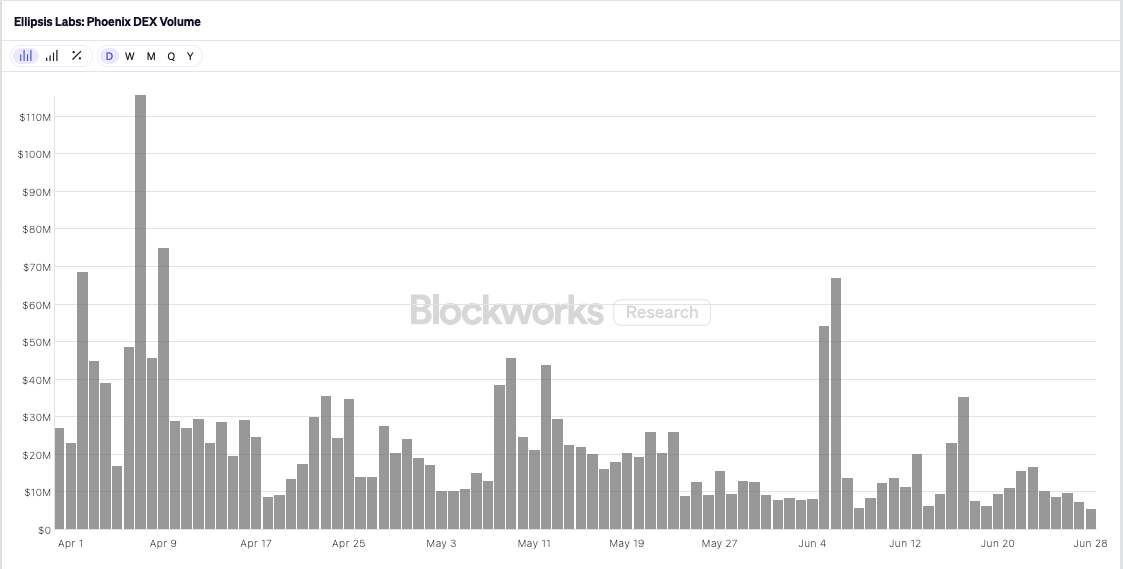

In late 2023, Ellipsis Labs announced Phoenix - a CLOB DEX that improved on Serum by achieving instant, atomic trade settlement without offchain cranking. Its architecture consolidates the orderbook, matching engine and trader balances into a single market account using efficient in-memory data structures. Its design minimizes account inputs, reduces compute usage, and achieves high throughput with subsecond finality. Phoenix primarily runs SOL/USDC and SOL/USDT pairs and even reached a daily volume peak of ~$1.2B early last year.

While Phoenix proves that a completely on-chain CLOB can operate on Solana, it still struggles because Solana’s architecture, despite being one of the fastest out there, isn’t fast enough for market makers to safely place tight bid/ask prices. When prices move quickly, market makers can’t cancel or update their orders in time, which means they often get stuck with bad trades and lose money. To avoid this, they either quote wider spreads (making the DEX less useful) or avoid it entirely.

Why Solana isn’t enough

Solana’s block production is paced by ~400ms slots, meaning order updates take hundreds of milliseconds to reach an optimistic confirmation (since currently, finality is ~12s). By contrast, high-frequency trading operates in sub-millisecond time. Market makers find that stale orders linger, so they must quote more conservatively to avoid being picked off. The single leader design also creates a bottleneck, where if the leader gets busy or censors transactions, all other updates, including cancels, wait, stalling order updates for ~400ms.

Solana’s fee market has also been unpredictable in the past, though improvements are being readily worked on. Market makers struggle to determine how much to bid for priority fees each time they update their quotes. This results in an unfavorable environment where market makers constantly overpay to avoid getting sniped. Traders are also forced to pay gas fees on every limit order, irrespective of whether it gets filled or not, leading to high operational costs.

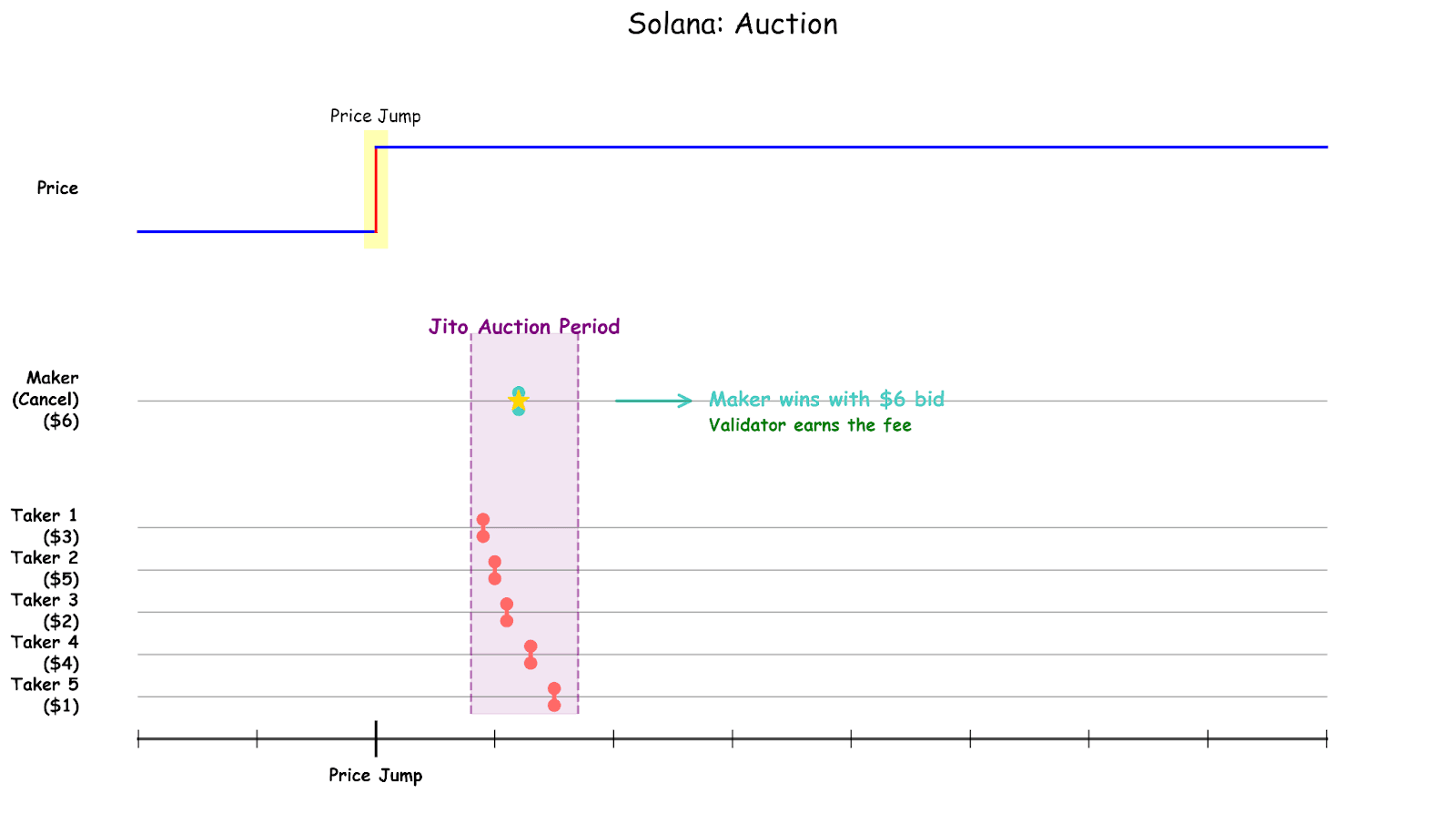

Another symptom of the single leader design is the Jito blockspace auction, making it impossible for market makers to win the race to cancel their quotes before takers can snipe stale orders. Even if the market maker is faster, what matters is who wins the blockspace auction. They can either pay a lot of money to cancel their quote, or they can let somebody else pay a lot of money to snipe them. This means market makers on Solana cancel orders successfully less often than on CEXs.

Finally, as a global distributed state system, Solana relies on the public internet to reach consensus, which is inherently noisy and delayed. Packets jitter, nodes lag, and blocks must reach all validators. This is unlike a centralized exchange, where all matching engines share one data center. These internet delays mean an order sent by a maker can be out of date by the time it’s confirmed on the network, further penalizing market makers who must quote conservatively. Most of the code behind DEXs and the network itself is also bug-ridden, which is a significant hindrance. This doesn’t mean CLOBs on Solana aren’t possible but it requires a level of understanding of the chain that very few people have.

Hyperliquid.

Late last year, Hyperliquid—a CLOB-based DEX — launched with its own hyper-optimized appchain and consensus algorithm, built from the ground up to power its enshrined order book. A high performance consensus algorithm (HyperBFT) and a colocated validator set enable block times of ~70ms. Hyperliquid charges no gas fees on orderbook transactions and prioritizes market maker cancels by automatically pulling all order cancels to the top of the block, mitigating the late-cancel problem faced on Solana CLOBs.

But at the end of the day, Hyperliquid is a permissioned consensus environment. It may be permissionless to use but if only a curated few run consensus, you’re operating under a delegated trust model that’s no longer censorship resistant. You’re effectively trading arguably the most important part of DeFi for lower latency. But in return, you don’t have to deal with game-theoretic complications. With no open-source code to publicly audit, you can’t even say if it’s just a Postgres instance running on AWS East-1.

This model may have valid engineering justifications, but censorship resistance is one of the biggest reasons onchain finance must succeed. Considering that Hyperliquid is closer to a CEX alternative than a blockchain, if Binance’s perps platform starts filling orders and allows permissionless access to the platform with a 50ms latency, that effectively nullifies their advantage. But at the end of the day, they do present a viable high-performance trading experience that Solana must seek to match.

Solana’s next moves

The Solana ecosystem has gone into war mode to ensure they are the victor in the CLOB battle. This has manifested itself as multiple approaches to solving the bottlenecks mentioned earlier in the article. Some of these approaches present a radical change to the protocol, and some are performance optimizations. These approaches include a brand new consensus protocol, steady upgrades to validator clients, multiple concurrent producers, and even network extensions. Jito recently released BAM (Blockspace Assembly Markets) to enable verifiable, private sequencing which could enable apps to prioritize maker orders and cancels.

Zeta Markets, a Solana perps DEX, announced their Testnet for Bullet, a low-latency ‘network extension’ (essentially an L2) in March, with mainnet launch planned in the coming months. By essentially creating purpose-built blockspace for orderbook transactions, you can have custom sequencing rules, for example, prioritizing cancels, latency as low as 2ms (soft finality claimed by Bullet), and throughput that’s orders of magnitude higher than what you see in general-purpose chains. While Bullet has its own custom blockspace and transaction execution model, it still relies on Solana for settlement, consensus, and data availability.

Solana’s founder Anatoly Yakovenko argues that an alternative execution layer for CLOBs are not beneficial to the base layer since they do not accrue any value back to it, and there is a general consensus among core contributors to the Solana network that network extensions are essentially a competitor to the base layer itself. He also argues that Solana can provide an L1-native solution that will require the newly announced consensus mechanism (Alpenglow), asynchronous execution, multiple concurrent producers and application specific sequencing on the base layer.

Alpenglow fundamentally revamps Solana’s consensus to achieve ultra-low latency(~97ms) on the base layer. It replaces Solana’s current Proof of History + TowerBFT consensus mechanism, which is the reason for subpar 12s finality and 400ms optimistic confirmations, and takes vote propagation off-chain, dramatically reducing consensus overhead.

Another pillar of Solana’s proposed approach is Multiple Concurrent Producers (MCP), which removes the single-leader bottleneck by allowing parallel block production. In the current single-leader model, only one validator at a time dictates the order of transactions for the entire network, limiting throughput and creating a central point of control. MCP instead enables multiple leaders to propose blocks simultaneously or in overlapping intervals, essentially creating parallel block streams that run concurrently. This parallelization enhances overall throughput and reduces latency by utilizing a greater portion of the network’s capacity simultaneously. It can also boost censorship resistance by preventing a single validator from monopolizing the network for the time period of a slot.

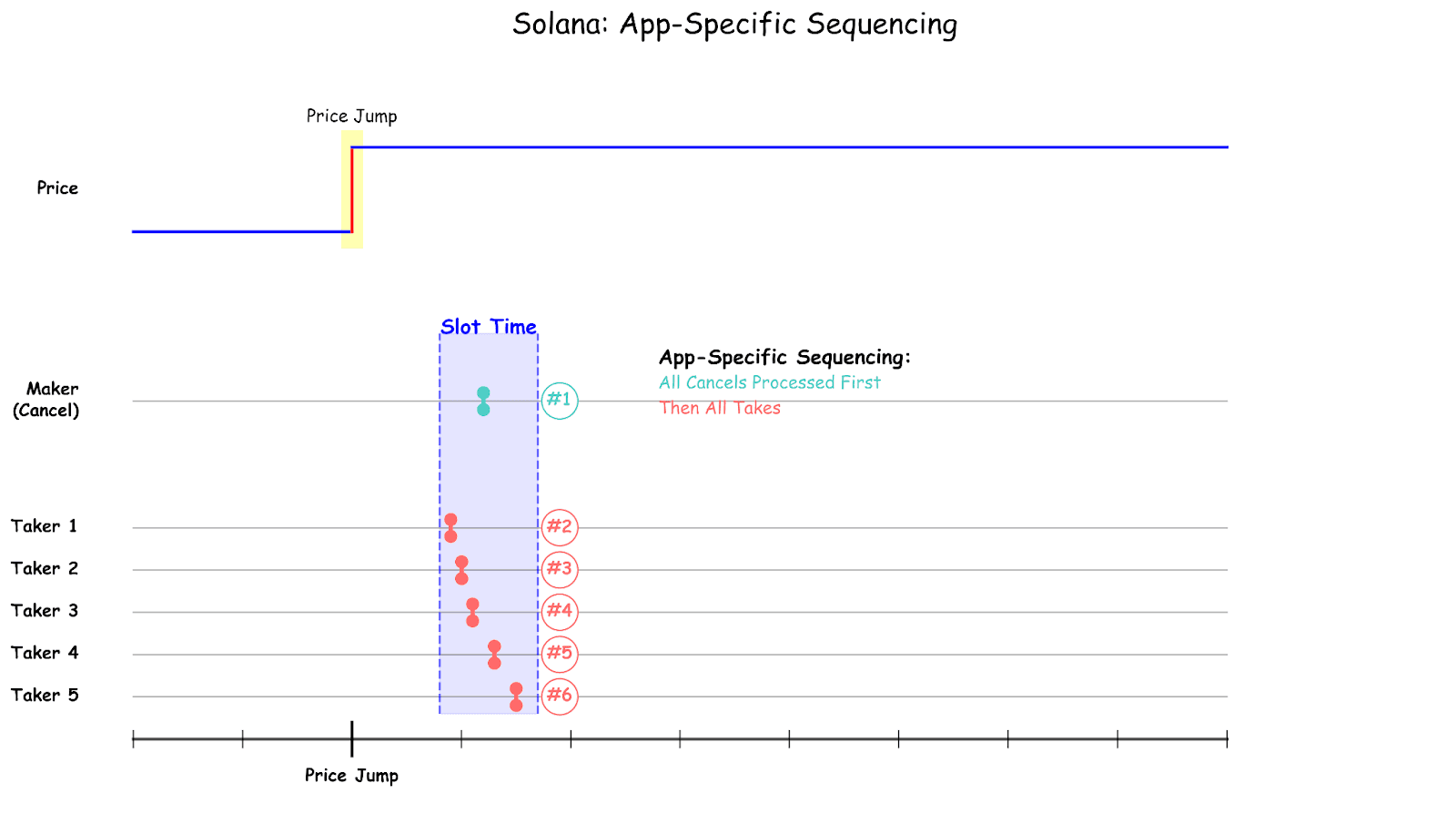

Finally, Asynchronous Execution and App-Specific Sequencing(ASS) work hand in hand to create specialized execution lanes with their own matching and prioritization rules. Asynchronous execution means consensus is reached on the order of transactions without immediately executing them, freeing up the consensus layer to finalize blocks much faster. App-Specific Sequencing lets particular programs or platforms define custom ordering logic within the base layer’s consensus rules. For example, an orderbook program could specify that order cancels receive the highest priority in their lane, ensuring market makers can quickly pull orders without delay. This roadmap aligns with Solana’s mission of outcompeting major stock exchanges and establishing a ‘decentralized NASDAQ’mbuspodma

Bottom Line

Hyperliquid is great at what it is — a permissionless CEX alternative, but does not possess the vital redeeming qualities of modern blockchains like censorship resistance and liveness guarantees. Solana aims to provide CEX-like performance with the security guarantees of a blockchain. Hyperliquid can be easily toppled by a centralized system that manages to be more performant, but building a blockchain with a permissionless validator set and optimizing it to beat trad-fi systems is much harder, but with the current progress in optimizing in the Solana network, I am optimistic that this will happen on Solana.